Always there for you

Certificate of Deposit Account Registry Service – CDARS

CDARS (Certificate of Deposit Account Registry Service) is one of the safest, smartest vehicles for investors looking to protect their large-dollar deposits while earning CD-level returns. CDs placed through CDARS offer:

• Access to multi-million-dollar FDIC insurance

• The ease of working through one trusted relationship, earning one rate per maturity, and receiving consolidated statements

• Relief from ongoing collateralization—because CDARS deposits are eligible for FDIC protection, you can eliminate ongoing collateral tracking

• A finite maturity date (in contrast to auction-rate or some adjustable-rate securities)

• The ability to have the amount of your deposit available to support lending initiatives that strengthen the local community *1

FREQUENTLY ASKED QUESTIONS

How can deposits greater than the standard FDIC insurance maximum ($250,000) be insured by the FDIC?

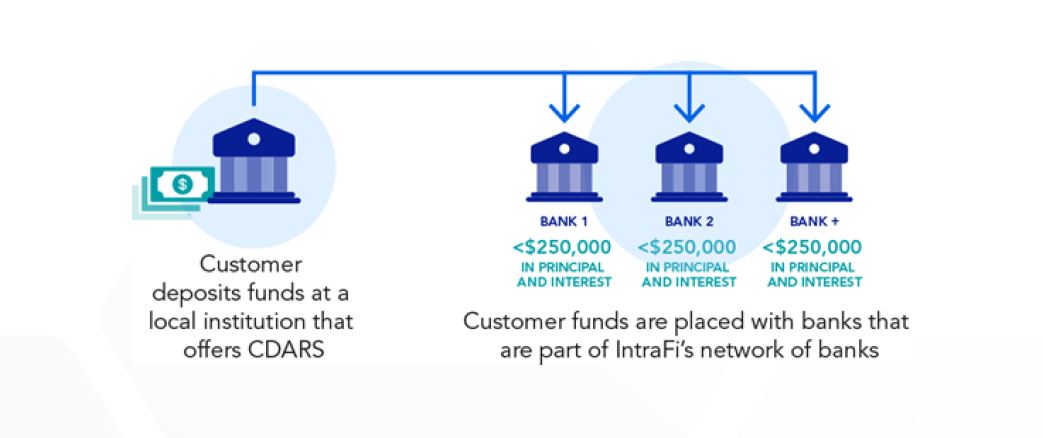

The standard FDIC insurance maximum is $250,000 per insured capacity, per bank. To protect a larger deposit, you could run around to multiple institutions to deposit your funds, or you could require a bank to collateralize your deposit and track changing collateral values on an ongoing basis. Alternatively, you can have us place your large-dollar deposit using CDARS. Your deposit is divided into smaller amounts and placed with other institutions that use CDARS, each an FDIC-insured institution. Then, those member institutions issue CDs in amounts under $250,000, so that your deposit is eligible for FDIC insurance at each member bank. By working directly with us, you can access coverage from many institutions while receiving a single regular statement.

Who has custody of my funds?

Funds placed through CDARS are deposited only into FDIC-insured banks. We act as custodian for your CDARS deposits, and the subcustodian for CDARS deposits is the Bank of New York Mellon (BNY Mellon). Unique to CDARS, you as a depositor can obtain a confirmation of records maintained by BNY Mellon as subcustodian to reconcile those records with the statements received from us. At any time, as often as desired, you as a depositor can obtain a certified statement from BNY Mellon that confirms the exact amount of your CDs, including principal balance and accrued interest, for each FDIC-insured institution that issues a CD through CDARS.

You can submit a request for the certified statement, along with BNY Mellon’s processing fee, through us. BNY Mellon will send the certified statement directly to you or to another party designated by you, such as an auditor.

How can my funds be used locally if my CDs are issued by financial institutions across the country?

When we exchange deposits with other institutions that use CDARS on a dollar-for-dollar basis, the same amount of funds placed through the network returns to us. As a result, the total amount of your original deposit can remain with our bank and be used for local lending. (CDARS Reciprocal transactions only.) *2

Is my account information safe?

You work directly with just us—the bank you know and trust. As always, your confidential information remains protected.

What happens if a CDARS institution that holds my deposit fails?

Most of the banks that have failed in the United States in recent years did not use CDARS or did not hold any CDARS deposits when they failed. When a CDARS institution has failed, the bank’s CDs issued using CDARS in most cases have been transferred to a healthy institution—the FDIC’s preferred method for handling bank failures. In cases where the FDIC has been unable to find a healthy institution willing to accept such a transfer, it has arranged for the payment of the insured principal and accrued interest to the depositors. This payment has usually occurred within a matter of days.

*1When deposited funds are exchanged on a dollar-for-dollar basis with other banks that use CDARS, our bank can use the full amount of a deposit placed through CDARS for local lending, satisfying some depositors’ local investment goals or mandates. Alternatively, with a depositor’s consent, our bank may choose to receive fee income instead of deposits from other banks. Under these circumstances, deposited funds would not be available for local lending

*2Deposit placement through CDARS or ICS is subject to the terms, conditions, and disclosures in applicable agreements. Although deposits are placed in increments that do not exceed the FDIC standard maximum deposit insurance amount (“SMDIA”) at any one destination bank, a depositor’s balances at the institution that places deposits may exceed the SMDIA (e.g., before settlement for deposits or after settlement for withdrawals) or be uninsured (if the placing institution is not an insured bank). The depositor must make any necessary arrangements to protect such balances consistent with applicable law and must determine whether placement through CDARS or ICS satisfies any restrictions on its deposits. A list identifying IntraFi network banks appears at https://www.intrafi.com/network-banks. The depositor may exclude banks from eligibility to receive its funds. IntraFi and CDARS are registered service marks, and the IntraFi hexagon and IntraFi logo are service marks, of IntraFi Network LLC.